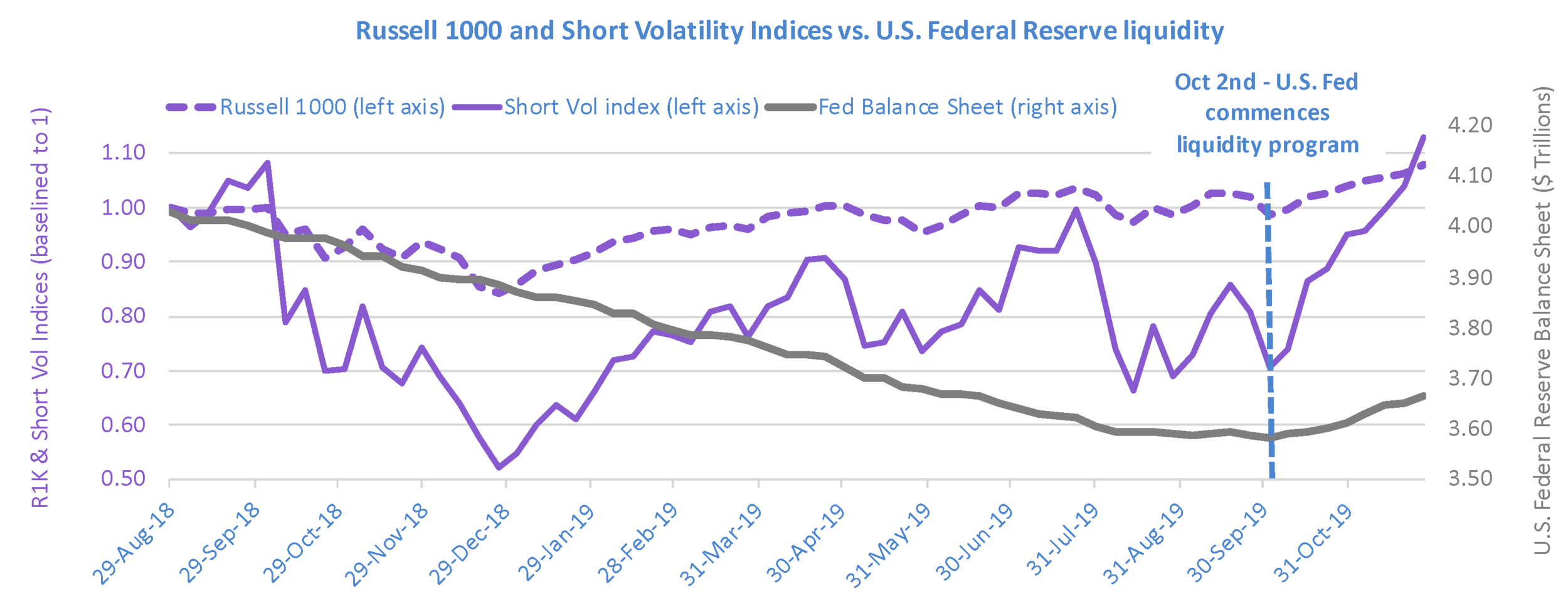

The first half of 2019 is a typical example of how our active portfolios can protect investors from behavioral biases that keep them from capturing stocks’ gains.

Recall the situation coming into the year. During the brutal selloff of 2018’s 4th quarter, the Huygens equity market stress indicator was bearish for 54% of the trading days. All the financial news was bad. It was frightening:

Given the turmoil, investors might have been tempted to exit all stock exposure to wait for clear signs that the economy has strengthened before getting back in.

Anyone doing that in 2019 missed a remarkable run and instead just locked in losses. The signs of strength didn’t come until after most of the gains had been earned – as is usually the case. In January, there was no all-clear signal in the news as headlines stayed bleak:

Even so, the S&P 500 gained +7.9% in January. The Huygens equity market stress indicator turned bullish within the first 5 trading days of the year, and as a result the most conservative Huygens active equity portfolio gained +3.7% while the most aggressive gained +5.6%.

In the months of February thru April 2019, economic news was mixed. An investor seeking unequivocal evidence of a strengthening economy still didn’t get it during these months, but equities kept recovering. The S&P 500 gained 8.9% from February through April, and because our equity market stress indicator stayed bullish throughout, our conservative active equity portfolio was up 5.0% and our most aggressive was up 6.7% in the same period.

Then came May. Headlines in the early part of the month finally made it clear that the previously expected 2019 recession had been averted:

But by the end of the month, news had turned sour again:

And the S&P 500 fell -6.6% in the month. Our active equity portfolio composition protected against much of these losses: our conservative portfolio clients lost only -0.5%, while those in our aggressive portfolio lost only -2.1%.

Once again, an investor might have taken May’s selloff as a sign the economy was really faltering this time, and again this would have been a mistake. Our equity market stress indicator stayed bullish throughout, positioning our active portfolios to capitalize on the gains that were to come in June as the S&P 500 established a new high.

The industry-standard way to assess the benefits of an active strategy such as ours is a metric called “capture.” Up-capture measures how much of an index’s gains our strategy delivered, and down-capture measures how much of that index’s losses our strategy gave up.

The below table shows that over the past nine months (Oct 2018 thru Jun 2019) of heightened stock market volatility, all three of our active equity portfolios delivered much more of the upside than the downside of the equity indices they actively trade (click here for comprehensive performance tables and index descriptions):